You Get Paid in USDT. Why Are You Still Struggling to Spend It?

You have USDT. You have bills, customers, invoices, purchases, and business needs. There should not be a thirty-minute detour standing between them.

Picture this.

It is a Tuesday evening. You just finished a design project for a client based in the United Kingdom. The invoice was $350. The client pays on time, which you appreciate, and sends the payment in USDT because that is the easiest way to move money across borders without losing a significant chunk to bank fees.

You check your wallet. The USDT is there. You feel good.

Then suddenly your light runs out, and you need to recharge your electricity before 9pm because you have a football match to watch at that time.

You open your phone. Check the time. It is 7:43pm. You have enough money. It is sitting right there in your wallet. But getting it from your wallet to a DISCO payment takes you through a process you have done so many times it feels like a second job.

You open your P2P app. You search for a USDT buyer. You find one, but their rate is lower than what you want. You find another. You initiate a trade. You wait for them to confirm. They take eight minutes to respond. You transfer the USDT. They send the naira. You check your bank app. The transfer is there. You open a bill payment app. You enter your meter number. You pay. You get your token.

It is 8:51pm. You made it. Barely.

And you will do this exact same thing next week when your data finishes. And the week after when you need to renew your DSTV subscription. And every single month for the rest of your life if nothing changes.

This is not a story about crypto being complicated. This is a story about infrastructure that was never built for the people who need it most.

The Irony of Being Crypto-Rich and Payment-Stuck

There is a particular irony in the situation that millions of Africans find themselves in right now. They have access to one of the most efficient forms of money ever invented. They can receive USDT from a client in London in under a minute. They can store value in a stablecoin that does not lose purchasing power the way naira does. They can transact across borders without a bank account.

And yet, when it is time to pay their electricity bill, they are slower than someone paying with cash at a shop.

This is not because crypto is broken. The technology works exactly as it should. The problem is that nobody built the last mile. The part that connects your USDT to the payment systems that the utility companies, telecom operators, cable providers, and other everyday service providers actually use.

Instead, what was built was P2P marketplaces. These are useful tools and they serve a real purpose. But they were designed for trading, not for bill payments. Using them to pay your monthly bills is a bit like using a wholesale market to do your daily grocery shopping. It works, but it was not designed for that, and you feel the friction every single time.

Let's Be Honest About What P2P Costs You

Most people who use P2P regularly have accepted the friction as normal. It has been the only option for so long that the inconvenience has started to feel like just the way things work. But if you actually stop and count what the process costs you, the numbers are more uncomfortable than you might expect.

Start with time. A typical P2P transaction, from opening the app to receiving naira in your bank account, takes between fifteen minutes and an hour depending on how responsive the buyer is, how quickly the bank transfer processes, and whether anything goes wrong. If you make four bill payments per month, which is conservative for most people paying electricity, airtime, data, and cable, you are spending somewhere between one and four hours every single month just on the conversion step alone.

That is time you are not working. Not resting. Not doing anything productive. You are sitting in a waiting room that should not exist.

Then there is the rate. P2P rates are almost never the best available rate. Buyers on P2P platforms are also trying to make money. The spread between the real market rate and what you get on P2P might be small per transaction, maybe one to two percent, but it is real money leaving your pocket. On a $200 USDT payment, that is two to four dollars gone. Every time. Across a year of payments, for an active crypto user, this adds up to a meaningful amount.

And then there is the risk. P2P trading requires trust between people who are usually strangers. Most platforms have escrow systems that protect both parties, and most transactions complete without incident. But scams happen. Disputes happen. Platform downtime happens at the worst possible moments. Every P2P transaction carries a small but real amount of risk that a direct payment simply does not.

You are paying a tax on your own money every time you go through P2P. A time tax. A rate tax. A stress tax. And none of it is necessary.

The People This Affects Most

It is worth being specific about who carries the heaviest burden from this infrastructure gap, because it is not evenly distributed.

Freelancers and remote workers who earn in crypto are at the sharp end of this problem. They are the ones whose income arrives in USDT or USDC and whose bills are denominated in naira. Every single payment they make requires a conversion step. For someone billing $3,000 a month and making ten to fifteen bill payments, the P2P process is a constant, recurring drag on their time and earnings.

Crypto traders who hold significant balances also feel this. When you hold USDT as a store of value and need to pay ordinary bills, you should not have to liquidate through a marketplace every time. It breaks the logic of holding the asset in the first place.

People who receive remittances in crypto are another group. A father in Abuja whose child in Canada sends money via USDT because bank transfers are slow and expensive should not have to navigate a trading platform every time he wants to pay school fees or restock the house.

And beyond these specific groups, there is a much larger, quieter category: ordinary Nigerians who got into crypto during the last few years, who have some USDT or Bitcoin sitting in a wallet, and who would use it more actively if using it was not so inconvenient. These are people who would genuinely benefit from a simpler way to spend their holdings, but the friction of the current process keeps them from doing so.

What Should Actually Happen

Let us describe what a properly built spending experience should look like for a crypto holder in Nigeria.

You open one app. You see your available balance in USDT, USDC, or Bitcoin. You choose what you want to pay for. Electricity. Airtime. Data. Cable TV. Betting. Travel. Food. Clothing. Government payments. You enter the details. You confirm. The payment goes through. Your balance updates. Done.

No switching between apps. No finding a buyer. No negotiating a rate. No waiting for a bank transfer. No checking your account three times to make sure the naira arrived. Just the payment, directly executed, in seconds.

The rate should be transparent and locked at the moment you initiate the process, not subject to change while you are waiting for someone on the other end to confirm. If a payment fails for any reason, your balance should be automatically restored. There should be no way to lose money to a technical failure.

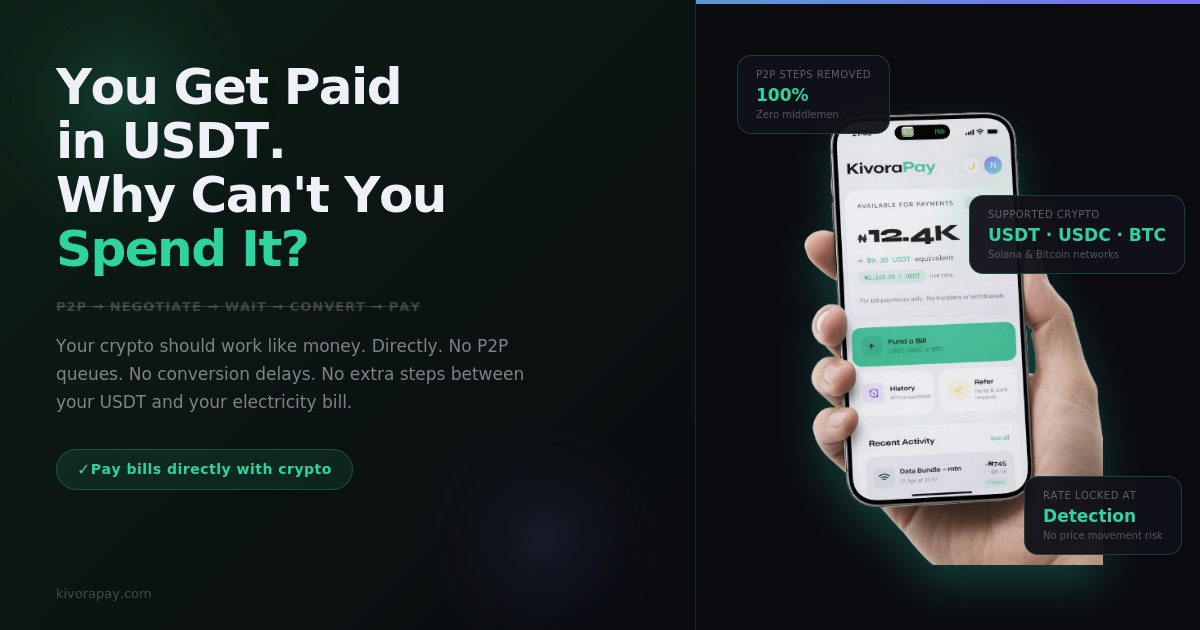

This Is What KivoraPay Is Built For

KivoraPay exists because this bridge needed to be built and was not.

When you deposit USDT, USDC, or Bitcoin into your KivoraPay account, your rate is locked the moment your transaction is detected on the blockchain. For USDT and USDC, your payment value is available almost instantly. For Bitcoin, it is available after two confirmations, which typically takes between ten and thirty minutes. And then you pay. Electricity, airtime, data, cable TV, betting accounts, and more. All from one place.

No P2P marketplace. No hunting for a buyer. No rate negotiation. No waiting for a naira transfer to land in your bank before you can make the payment you wanted to make in the first place.

The conversion margin is 1.5 percent for USDT and USDC and 2 percent for Bitcoin. That is the only fee. There is no subscription. No transfer fee. No hidden charges. Just a straightforward margin that is disclosed before your value is credited.

You worked for that USDT. You should be able to use it without a thirty-minute detour every time you need to pay a bill.

If a bill payment fails for any technical reason, your available balance is automatically restored. You cannot lose your money to a system failure.

The Bigger Picture

The struggle to spend USDT on everyday bills is not just an inconvenience. It is a signal that a layer of financial infrastructure has been missing from the African market for too long.

Crypto adoption happened fast in Africa because people needed it. The next thing that needs to happen, and that is now beginning to happen, is the building of the tools that make that crypto genuinely useful in daily life and business. Not just as a store of value or a trading instrument. As money that you can actually spend, receive, collect, and manage.

Every freelancer who gets paid in USDT and has to fight through P2P to pay their bills is experiencing the infrastructure gap in real time. Every trader who holds stablecoins but has to convert before every payment is experiencing it. Every remittance recipient who gets crypto from family abroad and then has to navigate a marketplace before they can buy groceries is experiencing it.

That experience should not have to continue. The infrastructure is now being built. The bridge is being laid. And if you have USDT sitting in your wallet and bills sitting on your table, you no longer have to go through four steps to connect those two things.

One app. Your crypto. Your payments, invoices, collections, and bills. Directly connected.

KivoraPay lets you spend, receive, and manage crypto-backed value across payments, bills, invoices, and business tools. No P2P. No waiting. No hidden fees.

Get Started Free