Africa Adopted Crypto. Nobody Built the Infrastructure to Spend It.

Africa has some of the highest crypto adoption rates in the world. KivoraPay is building the spending and business payments layer that makes those digital assets useful in real life.

Somewhere in Lagos right now, a freelancer just received $200 in USDT from a client in Toronto. The project took three weeks. The client paid on time. The work was good.

But the freelancer's electricity is about to go out.

Not because he does not have the money. He does. It is sitting right there in his wallet. The problem is that his electricity distribution company does not accept USDT. Neither does his cable TV provider. Neither does his airtime vendor. To use the money he just earned, he has to leave his crypto app, open a P2P platform, find someone willing to buy his USDT, negotiate a rate, wait for the buyer to send naira, and then finally go and pay his bill.

By the time all of that is done, thirty to sixty minutes have passed. Sometimes more. And this is not a one-off situation. This is every single time.

Africa did not fail to adopt crypto. Africa adopted crypto and then hit a wall built out of missing infrastructure.

This is the real story of crypto in Africa. Not the story of adoption, because that part already happened. The story that nobody is telling loudly enough is what happens after adoption. What happens when you have crypto but the world around you has not caught up. What happens when you are holding value that you cannot actually use.

The Adoption Numbers Tell One Story

By almost every metric, Africa has embraced cryptocurrency faster and more organically than most of the world. Nigeria consistently ranks in the top five countries globally for crypto transaction volume. A 2024 report noted that Nigerians owned 73 percent of all the cryptocurrency held on the continent. Ghana, Kenya, and South Africa are not far behind.

This did not happen because of marketing campaigns. It did not happen because a government policy encouraged it. It happened because people needed it. The naira has lost significant value over the past decade. Sending money home from abroad through traditional banking costs a painful percentage in fees and takes days. International clients paying African freelancers cannot easily send naira, but they can send USDT in seconds. The blockchain does not care about borders. It does not ask for a SWIFT code.

So people figured it out themselves. Young Nigerians learned how to set up wallets. They learned the difference between networks. They started receiving salaries in stablecoins. They figured out how to trade. Millions of ordinary people, without any formal financial education in crypto, became competent users of digital assets out of pure necessity.

That is remarkable. That is real adoption.

But the Spending Infrastructure Never Came

Here is what did not happen alongside that adoption. The tools that allow people to spend their crypto on normal everyday things did not get built. At least not in Africa, and not for the things Africans actually need to pay for.

Think about what a typical Nigerian household spends money on every single month. Electricity. Airtime. Data. Cable television. Rent. Food. School fees. Transport. These are the bills that make up daily life. None of these accept crypto directly. Not one.

So the question becomes: if you have USDT and you need to pay your DSTV subscription, what do you do? The answer, for most people, is P2P. You go to a peer-to-peer platform, you find someone willing to buy your USDT for naira, you agree on a rate, you wait for the transaction to complete, and then you go and make your payment.

This process works. But it is deeply inefficient. And the inefficiency is not small. It is real time, real stress, and real risk embedded into something that should be as simple as tapping a button.

The infrastructure gap is not about whether Africans can hold crypto. They can, and they do. It is about whether they can spend it without jumping through three additional hoops first.

What the Infrastructure Gap Actually Costs

The costs of this missing infrastructure are not abstract. They are felt every day by real people in concrete ways.

Take time. A P2P transaction in the best case takes fifteen minutes. In the worst case, the buyer ghosts you, the rate moves against you, or the bank transfer takes longer than expected. That is fifteen minutes to an hour spent on something that should take thirty seconds. Multiply that by every bill payment, every month, for millions of people. The cumulative time lost is staggering.

Then there is rate risk. The price you agree on in a P2P transaction is not always the price the market would give you. Buyers know you need to convert quickly, and some of them take advantage of that. The spread between the real rate and the P2P rate might seem small on a single transaction, but it adds up over time.

There is also counterparty risk. P2P requires trust between strangers. Scams happen. Disputes happen. Most platforms have escrow systems that reduce the risk, but they do not eliminate it. Every P2P transaction is a small gamble on the other person's reliability.

Why This Gap Exists

The infrastructure gap exists for a few reasons that are worth understanding. First, most payment infrastructure for everyday bills in Africa was built for naira and similar local currencies. The systems that utility companies, cable providers, and telecom operators plug into were designed for fiat money. Connecting those systems to crypto requires a bridge that nobody has built at scale.

Second, the regulatory environment in Nigeria has historically been uncertain for crypto. The Central Bank of Nigeria restricted crypto-related banking activity in 2021, which created a chilling effect on investment in crypto infrastructure. The situation has improved significantly since then. The CBN reversed its position, and Nigeria's Investments and Securities Act of 2025 formally recognises digital assets as securities. But the regulatory uncertainty of previous years slowed down the building of the infrastructure Africa needed.

Third, most global fintech innovation has not been designed with Africa's specific needs in mind. When Silicon Valley builds a crypto product, they are usually thinking about DeFi protocols, NFT marketplaces, or institutional trading tools. They are not thinking about how a freelancer in Ibadan is going to pay for airtime with the USDT they just received from a client in Berlin.

The gap was not created by laziness or lack of interest. It was created by a combination of regulatory uncertainty, geographic distance from where innovation was happening, and a fundamental mismatch between what was being built and what was actually needed.

What the Infrastructure Should Look Like

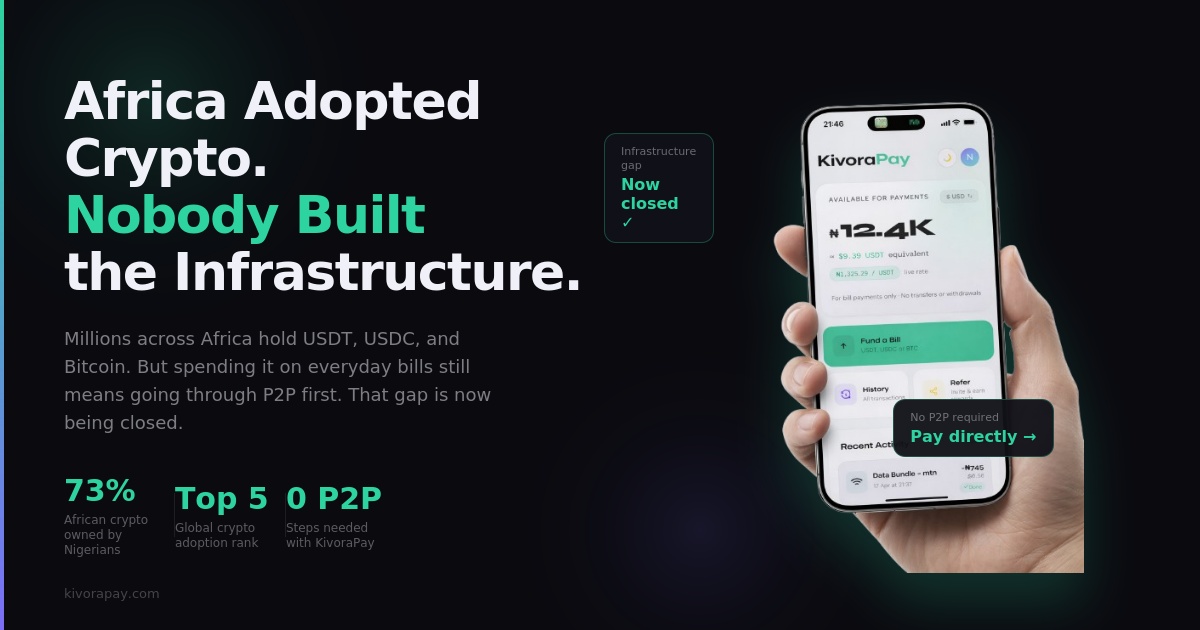

The solution to the infrastructure gap is not complicated in concept, even if it requires real work to execute. It looks like this: a user holds crypto, they want to pay a bill, they pay the bill directly with their crypto. No P2P step. No manual conversion. No extra hoops.

What makes this possible is a layer that sits between the user's crypto wallet and the licensed payment infrastructure that processes bill payments. That layer handles the conversion in the background, connects to the payment aggregators, and delivers the payment to the relevant provider. The user just sees a simple interface where they can choose what they want to pay for.

This is not science fiction. The technology to do this exists. The licensed payment aggregators that handle bill payments in Nigeria exist. The crypto rails exist. What was missing was someone putting the pieces together in a way that is designed specifically for the African user.

This Is What KivoraPay Is Built For

That is exactly what KivoraPay is built to do. It is a spending layer for crypto: a way for people and businesses to use digital assets for payments, collections, invoices, commerce, payroll, payouts, and everyday transactions. No P2P. No conversion stress.

The Opportunity in the Gap

Every infrastructure gap is also an opportunity. Africa's crypto adoption happened without the tools to make that crypto useful for daily life. The people who build those tools are not just solving a problem. They are building the foundation of a new financial layer for an entire continent.

The numbers support the scale of this opportunity. Nigeria alone has tens of millions of crypto holders. If even a fraction of them switch from manual P2P conversion to a direct spending and business payments layer, the transaction volume is significant. Add Ghana, Kenya, South Africa, and the rest of the continent over time, and the scale becomes genuinely large.

The infrastructure is now being built. The bridge is being laid. And for millions of crypto holders across Africa, the wait for a simpler, more direct way to spend their digital assets is finally coming to an end.

Africa adopted crypto on its own terms, without waiting for permission or infrastructure. Now the infrastructure is catching up. And that is when things get interesting.

KivoraPay is the spending layer for crypto holders and businesses in Africa. Spend, receive, collect, invoice, and operate using crypto-backed value. No P2P. No waiting.

Get Started Free